The Coalition’s Santiago Action Plan stresses the importance of incorporating climate change considerations into financial decisions and identifying risks climate change poses to financial stability. In this context, the Coalition produced this note on climate-related financial risk to raise awareness and explore risk management approaches. The findings of this note will be reviewed by Coalition Members with a view to identify policy priorities and potential areas for future work.

This note provides an overview of how climate-related risks may manifest in different sectors of the economy and alter macroeconomic conditions that affect the work and responsibilities of Ministries of Finance (MoFs). The interaction of various risks may lead to reinforcing feedback effects that could gradually or abruptly cause high fiscal costs and trigger contingent liabilities of MoFs with growing climate change. However, the materiality of these risks – posing potentially high ex-ante unknown fiscal costs for MoFs – depends on the interplay of climate-related risk transmission channels, the degree of unfavorable reinforcing feedback loops, the specific country context, and climate action measures.

Ambitious mitigation and adaptation measures could reduce the likelihood of severe climate-related risk impacts that could otherwise grow and potentially hinder countries’ long-term economic development. The note concludes with potential policy actions MoFs can take to mitigate and manage climate-related risks.

Download: Climate-Related Risks for Ministries of Finance: An Overview

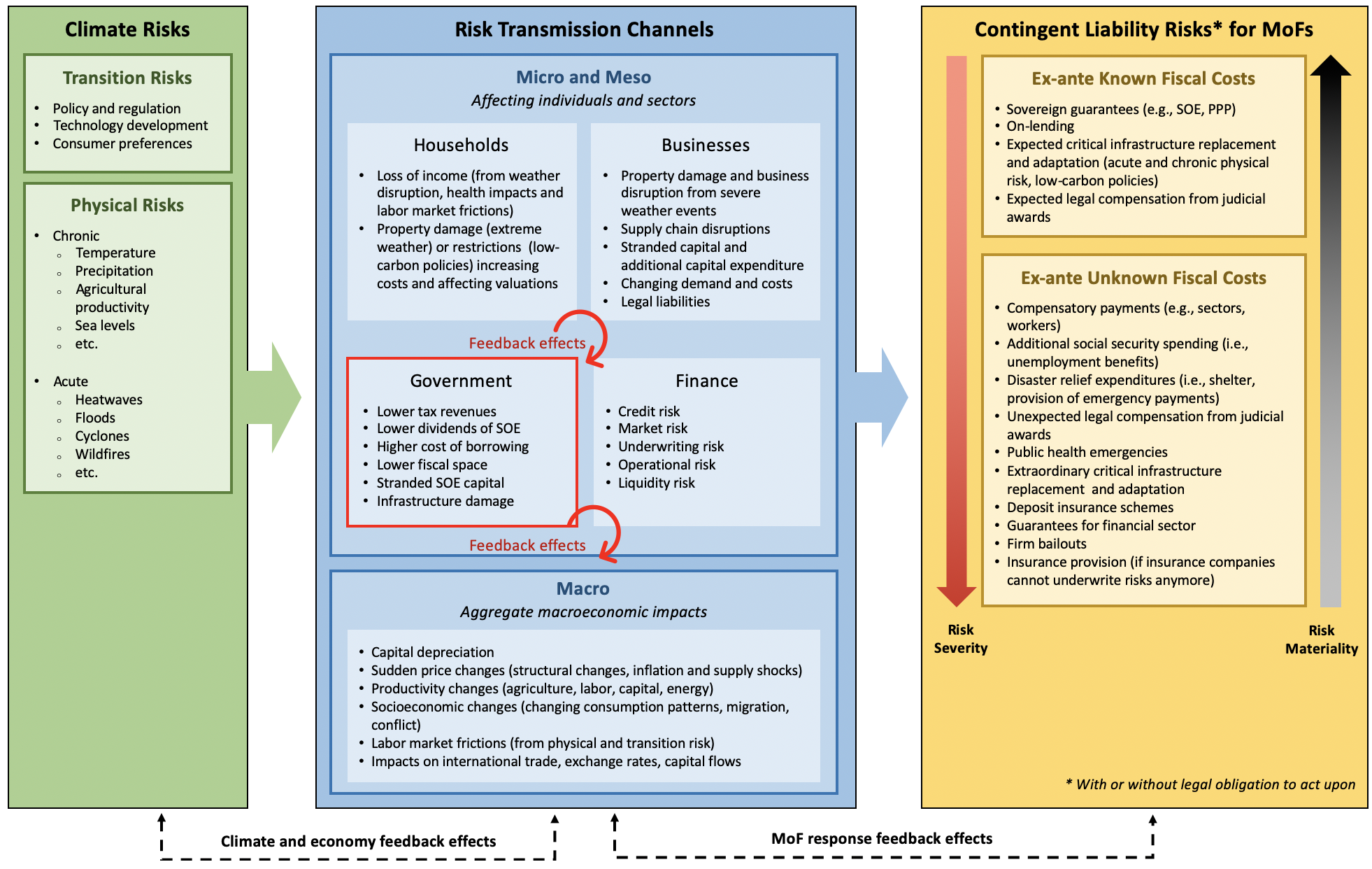

Below is a key graphic from the report:

Climate-related risk transmission channels and Ministries of Finance

Note: The figure shows the transmission of climate-related risks (physical or transition) to different sectors of the economy (including government fiscal risk) and the macroeconomy. The interaction of these risks may lead to reinforcing feedback effects – potentially triggering contingent liabilities of the MoF. Contingent liabilities are defined as obligations that only materialize when a certain event in the future occurs. Contingent liability risks could become gradually or abruptly more severe with ongoing climate change (depending on the specific country context), as indicated by the red “risk severity” arrow. However, the materiality of these risks, posing potentially high ex-ante unknown fiscal costs for MoFs, depends on the interplay of climate-related risk transmission channels, the degree of unfavorable reinforcing feedback loops, and climate action measures – as is indicated by the grey “risk materiality” arrow.

Source: Authors’ conceptualization adapted from NGFS (2020), Schuler et al. (2019), Volz et al. (2020) and IMF (2008)